What Gen X Can Do To Save Their Retirement

Arecent report highlights that many Gen Xers’ retirement savings are woefully short of what they will need to be income secure for their retirement years.

Let’s look at the problem and some steps they can take to not reach their retirement years with worries about making ends meet.

This month, the National Institute on Retirement Security published a report titled: “The Forgotten Generation: Generation X Approaches Retirement,” focusing on the 64 million Americans born between 1965 (age 58) and 1980 (age 43).

Generation X was the first group to enter the workforce as employers dropped defined benefit pension plans and replaced them with contributory 401k plans. While defined benefit plans provided a predictable level of retirement income, 401k plan outcomes are subject to how much employees contribute and the swings of the financial markets.

The report included both individual averages and household numbers; I’m choosing to focus on the household savings results.

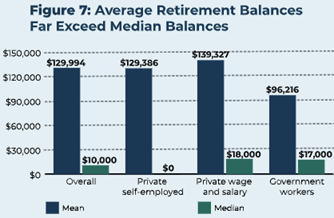

The report shows the average Gen X worker has retirement savings of about $130,000. However, the median amount is just $10,000. This means half of Gen X workers have less than $10,000 in their retirement accounts.

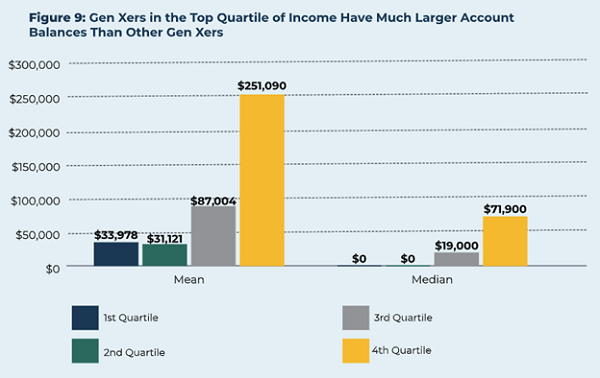

By income, the large majority of retirement savings is held by the top quarter by income of wage earners. You can again see the massive discrepancy between average and median amounts of retirement savings.

The report uses retirement savings targets published by Fidelity. The guidelines recommend these retirement savings levels:

- Age 40: 3 times annual income

- Age 45: 4 times income

- Age 50: 6 times income

- Age 55: 7 times income

- Age 60: 8 times income

- Age 67: 10 times income

According to the National Institute on Retirement Security report that 85% of Gen Xers have less than 50% of the recommended target, and about 60% have less than 10%. These are frightening numbers, and if you are a member of Generation X, you will likely need to formulate a plan to boost your retirement savings or plan on working until well into your 70s.

However, it is not hopeless. If you start now, there are steps you can take to build up your retirement savings more quickly.

First, make sure you participate in your employer’s 401k plan. Again, according to the report, only 55% of Gen X workers participate in employer-offered retirement plans. Most plans offer employer matching funds, so as you defer some of your income, your employer will match with additional savings dollars. If you are self-employed, you can set aside significant retirement dollars by starting a simplified employee pension (SEP) or solo 401k.

You should also fund a traditional IRA or Roth IRA. Both are tax-advantaged in different ways. Depending on your income and retirement plan at work, traditional IRA deductions can reduce your taxable income. IRA earnings grow tax-deferred. Roth IRA contributions do not reduce your taxable income but grow tax-free. Roth earnings are never taxed. For 2023, if you are under 50, you can contribute $6,500 to either type (total contributions); if you are over 50, you can put away $7,500.

If you max out IRA contributions, open up a regular brokerage account, and start to add money. You can invest in stocks, ETFs, and money market mutual funds in a brokerage account. If you know you are way behind in your retirement savings and want to get more money working, start or add to a regular brokerage account.

This post originally appeared at Investors Alley.

Category: Personal Finance