11 Financial Tips For Parents To Share With Their Kids (Part 1)

As parents, we want the best for our kids. Most schools do not do a good job of teaching personal finance. Helping our kids become more financially savvy can help us have a lasting impact on their lives. It can also allow them to live the lifestyle they desire.

It starts with teaching them to be careful with their money. At its most basic level, this means being sure they decide to save at least a portion of their income. It includes living within or below their means. It also involves helping them understand the value of using credit cards wisely and not paying credit-card interest. While some kids may be minimalists – like my two oldest – others may tend to accumulate unnecessary things.

1. Learn self-control – create a budget.

Help your children learn the art of delaying gratification. It can be easy to purchase an item simply because you want it. Self-control allows you to wait until you can pay for/afford something. Paying credit-card interest on items such as clothing or personal electronic items makes them more expensive in the long run. It can also destroy long-term wealth.

2. Pay yourself first.

When it comes to saving, remember these three words. If you are not familiar with the term, when you “pay yourself first” you automatically route a specified savings contribution from each paycheck to a specific savings or investment account upon receipt. Because your savings contributions come before you even see or touch your money, you are paying yourself first. You pay yourself by saving a portion of your income. You do this before you start paying your monthly living expenses and making discretionary purchases. Paying yourself first helps remove the temptation to skip a contribution and spend your money rather than build your savings. Please see this blog for more detail about this topic.

3. Start saving early – Open a Roth IRA as soon as you can.

Time in the market matters much more than timing the market. Investing for longer time frames allows your money to grow. The more years it can grow, the more potential there is for it to increase to a large sum. I discussed the importance of starting to save early in this blog. I also shared an article that reviewed the concept last week.

If possible, have your children open a Roth IRA as soon as they start working. This applies even if they get their first job in high school.

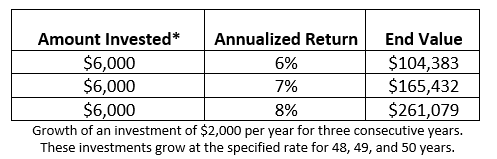

If you can, consider funding the Roth IRA for your child. Early in their career, their tax rate will likely be low as they haven’t yet maximized their earnings. You don’t pay taxes on the growth in a Roth IRA. You also don’t pay taxes when you make withdrawals. Consider what happens if they Invest $2,000 a year in a Roth IRA from ages 18-20 and keep it in their Roth until they reach age 68. The table below summarizes how much small investments can grow over time.

4. Take advantage of the company match.

If the company you work for has a retirement plan such as a 401k with a company match, contribute at least enough to earn the match. Your company match represents part of your compensation. If you don’t accept it, you’re choosing to accept a lower rate of pay. You’re also passing up additional growth in your investments. A common match is 50% on the first 6% contributed. This means if you contribute 6% of your salary, your total contribution equals 9%. This match increases your contribution by 50%.

Additional benefits come when you regularly contribute to your company retirement plan. First, this represents a way to “pay yourself first” – see #2 above. Second, it allows you to contribute to the market whether stocks are going up or down. Adding money when the market falls is hard. But if you have a long time horizon, it’s a path to success. It allows you to buy more shares of the same security when the market falls. That will work to your benefit.

5. Plan for the future – set goals.

If you want to achieve financial success you must set goals. Why? You should know what you’re saving for and why.

Goals can include any or all of the following. buying a house or car, going back to school, starting a family, funding your child’s education, or saving enough to allow you to retire early. Knowing your goals gives you a better idea of how much you need to save. It can also help you create a plan that will help turn your dreams into reality.

Remember that goals, especially monetary ones, can change. That’s why when we work with clients on financial plans, we remind them that the path from “Retirement Uncertainty” to an “Informed Retirement” is not a straight line. It can and should be updated when your goals and/or circumstances change.

6. Understand taxes.

You want to understand how income taxes work before you receive your first paycheck. When you get a job offer, you want to have an idea of whether that salary will leave you enough to live on. That means you want to understand how much you will pay in taxes and other obligations.

For example, $50,000 a year in Maryland will leave you with about $38,000 in net or take-home pay. If your salary increases to $60,000, you will have about $44,500 left. You can use this website to estimate your take-home pay.

You also want to consider ways in which you can reduce your tax bill. This includes putting money in tax-deferred retirement accounts such as IRAs or 401k’s.

Part 2 of this week’s blog will be published in two weeks. This article originally appeared at Apprise Wealth Management.

Category: Personal Finance