Silicon Valley Bank Default Rattles The Markets

Banking is relatively simple, they raise deposits and lend money. To do so successfully, a bank must manage a few risks. First, they need to duration hedge to address the difference between short-term deposit rates and the interest rate they lent money stays positive. Second, they hedge the credit and price risk of their assets. Lastly, and most importantly, they must keep deposits in the bank. The FDIC put Silicon Valley Bank (SVB) into receivership because it did not correctly hedge its loan/asset book. As a result, they took a $1.8 billion loss, scared depositors, and induced a bank run. As depositors pulled their funds, Silicon Valley Bank had to sell more underwater assets. Silicon Valley Bank is the second largest bank failure in the U.S., behind Washington Mutual in 2008.

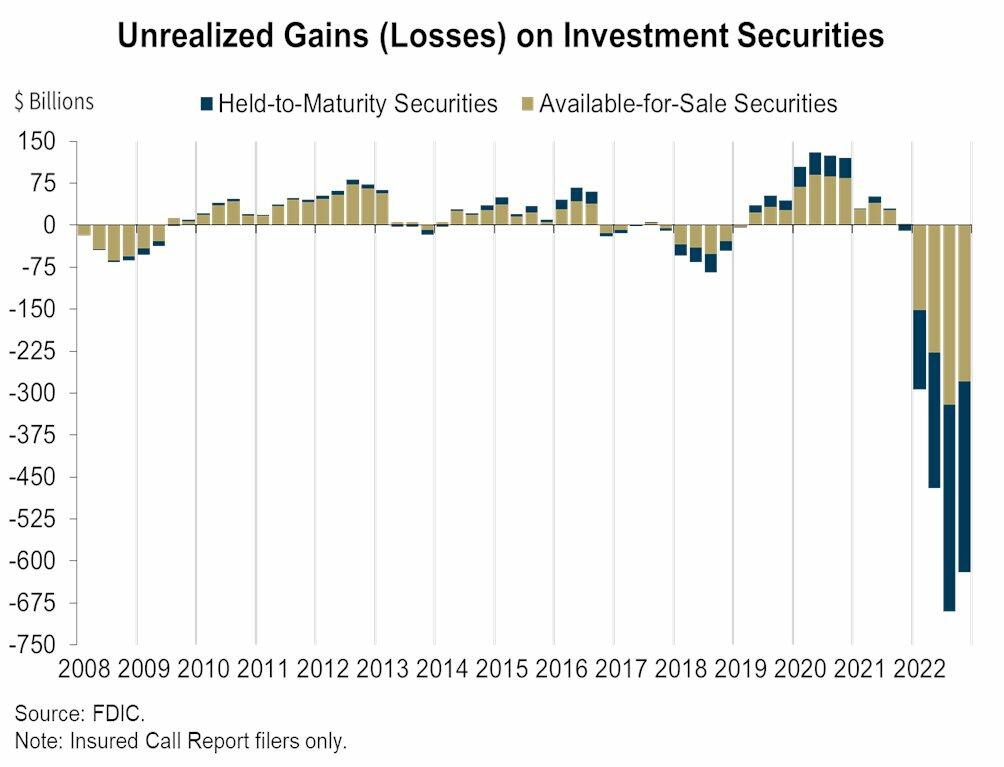

Banking is a confidence game. The problem facing Silicon Valley Bank and potentially others is that many assets are underwater due to the sharp increase in yields. Below, we dive into bank balance sheets to better explain SVB’s problem. Bank stocks, especially regional banks, are falling in sympathy with SVB. Investors are concerned that banks were not well enough hedged for the sharp rise in interest rates. Hence, they would have to recognize significant losses if deposits leave. Through 2022, banks are sitting on about $700 billion in losses.

Market Trading Update

The news that SVB Financial Group was forced into receivership by the FDIC panicked investors and sparked fears of a liquidity crisis amongst regional banks.

The crack in regional banks is likely only starting as the Fed continues to hike interest rates, leading to more underperforming loans and reduced funding. Unlike the big banks, which have access to capital markets and trading revenues to offset traditional banking incomes, smaller banks have exposure to real estate, consumer, and small business loans that are more sensitive to increased borrowing costs.

“Banks – and especially small banks – are now sitting with reserves pretty much at their lowest comfort level, There is not much of a cash-to-asset cushion left for small banks as a whole, so a funding crisis can easily get rolling if large depositors decide too many loans in commercial real estate and other areas are about to go bad. The Fed will make funds available to keep these banks afloat, but that alone will get some push-back from Congress because of the increased concentration of bank deposits in an increasingly smaller number of banks.” – Steven Blitz, TS Lombard

With that, the market took out the support at the rising trend line and the 200-DMA, which violated our stop-loss levels, where we reduced exposure to equities. With all of the previous bullish support levels broken, the next logical level of support is the December lows. A failure there will then set supports at the June and October lows.

The one-two punch of Jerome Powell and SVB has put the bears back in control of the market. Unfortunately, the problem for the regional banks, corporate earnings, and the market is likely starting to gain traction. Use rallies to reduce equity risk and add Treasury bond exposure.

Fed Bailouts Begin

Last night the Fed, FDIC and the Treasury made a joint statement to provide a liquidity facility for banks.

As the WSJ’s Ben Eisen recaps,

“The facility will allow banks to take advances from the Fed for up to a year by pledging Treasury’s, mortgage backed bonds and other debt as collateral.”

By allowing banks to pledge their bonds – not just at current market price but at cost (or at par) – banks can meet customer withdrawals without selling their bonds at a loss. Of course, that is what Silicon Valley Bank did last week, sparking a run on the bank.

Indeed, as Eisen underscores, the biggest draw of this facility is that “banks can borrow funds equal to the par value of the collateral they pledge, according to the Fed’s announcement. This means that the Fed won’t look to the market value of the collateral, which in many cases reflect big unrealized losses due to the jump in interest rates.”

That is a huge gift for the banks which are sitting on some $620 billion in unrealized losses on all securities (both Available for Sale and Held to Maturity) at the end of last year, according to the Federal Deposit Insurance Corp. It also means that just the Big 4 banks – as shown in the chart above – are getting a $210 billion bailout. – Zerohedge

The Fed also won’t demand that banks pledge collateral above the advances they are taking, which is typically the case when banks borrow from the Federal Home Loan Bank system for example.

And if banks can’t repay all the advances in a year? The Treasury Department is providing $25 billion of credit protection to the Fed just in case.

“The Federal Reserve does not anticipate that it will be necessary to draw on these backstop funds,” the Fed said in its announcement Sunday night.

That, in a nutshell, is how the bank bailouts have began.

The Week Ahead

CPI on Tuesday and PPI and Retail Sales on Wednesday will highlight economic data this week. After last month’s hot inflation prints, the Fed and investors could use weaker inflation figures. Monthly CPI is expected to rise 0.6%, a tenth higher than last month, and the annual rate is forecast to fall from 6.4% to 6.0%. After last month’s massive retail sales gains, forecasters expect a slight decline.

The Fed will be quiet this week as they are in their pre-FOMC meeting media blackout period. Consequently, we suspect they will speak through the Wall Street Journal if they have anything to say about monetary policy or the banking sector.

The BLS Jobs Report

Once again, payrolls grew by more than estimates. In February, 311k jobs were added versus forecasts of 225k. The unemployment rate did tick up to 3.6% from 3.4% because the participation rate rose to its highest level in three years. 419,000 people entered the labor force in February. The unemployment rate rose because more people were looking for jobs, not due to layoffs. If this continues, the growing workforce should help reduce job openings and bring the labor market back into balance. Such would weigh on wages and lower the risks of a price-wage spiral.

Average hourly earnings only rose 0.2%, and weekly hours worked fell by a tenth of a percent. The data, on its own, will do little to change the Fed’s decision on whether to increase rates by 25 or 50bps at the March 22 meeting.

Dissecting Bank Balance Sheets To Appreciate SVB’s Problem

We examine aggregated bank balance sheet data from the Federal Reserve’s H.8 report to understand Silicon Valley Bank’s default better. The pie charts below break down commercial banks’ aggregate assets and liabilities.

The banks’ asset side is predominately a portfolio of fixed-income securities and loans. Not all of the assets are liquid. Of the assets shown below, 47% can be quickly sold to raise capital/liquidity. Besides cash and potentially trading assets, most of the Treasury securities and MBS likely have significant unrealized losses. While the loans are not often liquid and, in some cases, not tradable, their values (prices) are also underwater. If a bank properly hedges, hedge gains should offset most current losses. However, as in the case of Silicon Valley Bank, they did not hedge properly. As a result, the combination of price markdowns and deposit losses left the bank with no choice but to have a firesale, recognize losses, and try to raise capital. They couldn’t raise enough capital and were put into receivership.

Deposits are the banks’ funding lifeline, accounting for over 85% of their liabilities. When a bank loses deposits, it must shed assets to keep its leverage and capital ratios in check. When assets are poorly hedged and underwater, they must sell more assets and take larger losses for each lost deposit. Such begets more deposits to leave, and a circular problem ensues.

The second graph below shows that banking deposits are falling for the first time in at least 45 years. Depositors are seeking much higher yields in money market funds and other alternatives. Bank stock investors are losing confidence as banks must sell assets to offset deposit declines, potentially entering into a death spiral like SVB if the bank did a poor hedging job.

Tweet of the Day

This post originally appeared at Real Investment Advice.

Category: Uncategorized

{kind=link}