No Rate Cuts In ’24? I’m Not Buying It (Here’s Why And How To Profit)

We’ve got a great shot at locking in big yields—and big dividend growth—on utility stocks. But we need to buy now, before rates start their (inevitable) decline.

I’ve got three “growth utilities”—boasting fast-growing businesses and dividends—for us to play this opportunity with below.

Best part is, thanks to their healthy balance sheets, these three have a built-in “buffer” if rate cuts do get held up for a bit.

Last October’s Rate Peak Was Just Act 1

I know this plan works because, well, it’s exactly what happened last fall, when fear was everywhere and the 10-year yield scraped up against the 5% barrier.

We didn’t buy the panic, though. We bought—including a dividend-growing utility that’s one of the best out there. But it’s rarely cheap because everyone knows it’s great!

That would be Florida-based NextEra Energy (NEE)—more on NEE below—which I named as a best buy from the portfolio of my Hidden Yields dividend-growth service in the October 2023 issue.

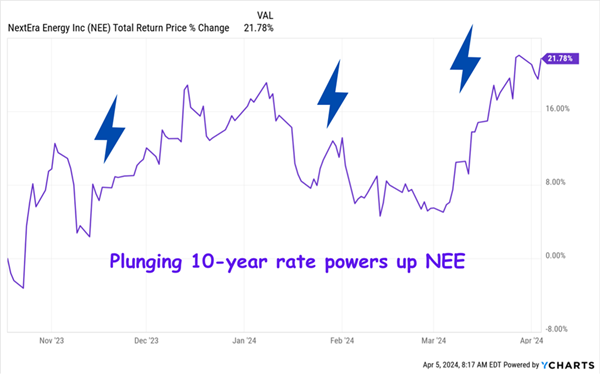

Just as we expected, the panic faded and the 10-year yield deflated to 3.8%. NextEra? It’s popped 22% (with dividends included) in the five-and-a-half months since the 10-year rate peaked on October 18:

NEE Soars Into ’24

So what now? With the 10-year Treasury ticking up—now around 4.4% after Friday’s strong jobs report—has our utility-buying opportunity shifted to the back burner?

No way.

To be sure, long rates might hover around these levels for a bit. But the Fed’s rate hikes will eventually add up, and the much-talked-about recession will arrive.

That will result in lower interest rates, both on the “short” end (controlled by the Fed) and the “long” (determined by the 10-year Treasury rate). As rates fall, the prices of bonds and “bond proxies,” like utilities, will pop.

In other words, now is the time to get in, before rates tip lower again. Now let’s dive into those three top utility picks for doing so.

“Growth Utility” Pick No. 1: NextEra Energy (NEE)

NextEra Energy is best known for its Energy division, one of the world’s biggest renewable-power investors, with 72 gigawatts in operation. The company also operates regulated Florida Power and Light, America’s biggest electric utility, with 34 gigawatts in operation and 5.9 million customers.

It’s a terrific business mix, with FPL providing about 70% of NEE’s business and NextEra Energy chipping in the remaining 30%. NextEra’s renewable business has even more growth “baked in” through its 20-gigawatt backlog of contracts.

Florida, as you no doubt know, is booming. Its GDP, at $1.5 trillion, makes it the world’s 14th-largest economy, ahead of Mexico and behind South Korea, according to the Florida Chamber of Commerce.

I’m sure you’ll agree that those are all impressive numbers. Yet NEE’s stock price languishes some 32% below its all-time highs.

What gives?

We can blame it on interest-rate hikes that, as we just discussed, are in the rear-view mirror. The closer we get to a recession and lower rates, the more we’ll see utility stocks, especially dirt cheap ones like NEE, rise.

And the stock is cheap by just about every measure. Its forward price-to-earnings (P/E) ratio is 18.7, far below its five-year average of 24.4. In other words, if I’m wrong and rates do stay higher for longer, we don’t have to worry. It’s already priced in!

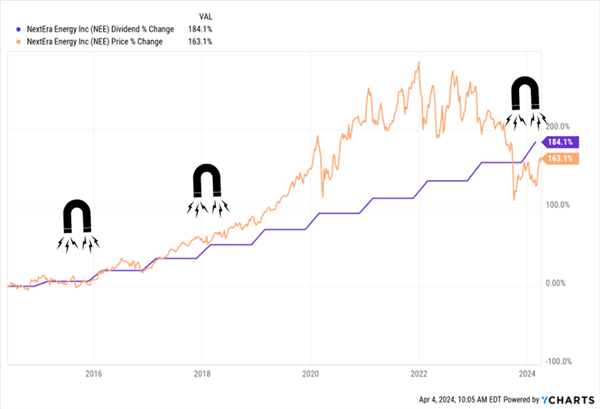

Then there’s the “Dividend Magnet”—the proven pattern of a company’s dividend growth pacing its payout higher over time. You can see it with NEE below—you can also see that the current lag (a rarity for NEE) signals a stock begging to be bought:

When NEE’s Stock Trails Its Payout Growth, We Buy

Finally, NEE’s debt is just 41% of assets—very reasonable for a utility and yet another reason we can be confident in this one, no matter what rates do.

“Growth Utility” Pick No. 2: Sempra (SRE)

Sempra (SRE), like NextEra, has a pretty sweet growth-and-stability setup. It’s rooted in California, which is growing faster than most folks think, with GDP up a healthy 3.1% in the fourth quarter of 2023, according to the Bureau of Economic Analysis.

But the real growth driver is its other main market, Texas, where it has 13 million customers and operates 143,000 miles of transmission lines.

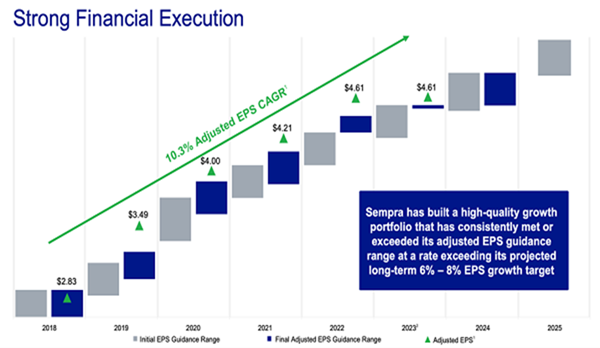

The state is, by any measure, en fuego, posting 5% GDP growth in Q4, topping even Florida at 4.6%. Then there’s Sempra’s own stellar earnings history: management continuously sets a 6% to 8% EPS-growth target … and continuously crushes it:

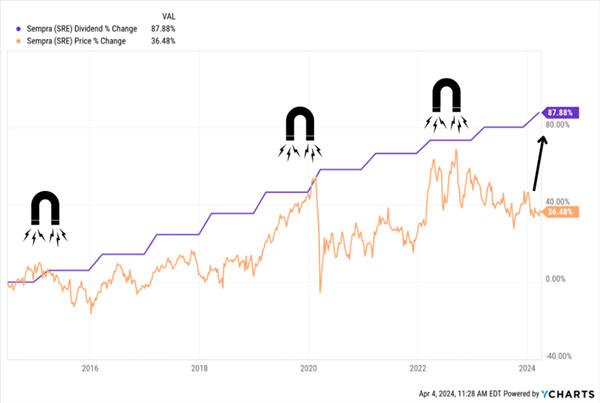

No wonder Sempra’s payout (current yield: 3.5%) is on a tear. And, as with NextEra, it’s pulled up the share price with it, with the same “lag” pointing to a buying opportunity:

Sempra’s “Dividend Gap” Shows Our Upside

The stock’s bargain status is backed up by its forward P/E: just 13.8—well below its five-year average of 15.5.

Finally, we’ve got a “fortress” balance sheet here, too, with long-term debt of $31 billion, lower than NEE at just 31% of assets.

“Growth Utility” Pick No. 3: Alliant Energy (LNT)

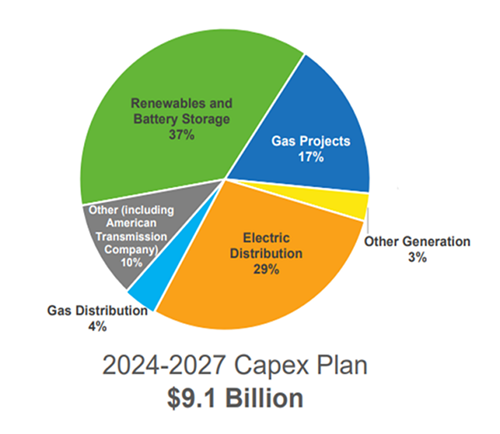

Alliant Energy (LNT) boasts a stable core of clients (995,000 electric customers and 425,000 gas customers in Iowa and Wisconsin). It also owns 16% of American Transmission Co., with 10,000 miles of transmission lines and 560 substations.

Alliant’s core markets put it in a great position to profit from two ongoing megatrends: the electrification of industry and the return of manufacturing to America.

Industrial consumers account for 31% of Wisconsin’s energy consumption, and the state has seen plenty of new factory announcements, including from Generac Holdings (GNRC), German confectionery maker HARIBO and a corrugated-box factory run by WestRock (WRK).

Alliant is building the capacity those businesses will draw on, mainly through renewables, with nearly 40% of its capex focused on wind, solar and battery storage.

That’s a smart move as the price of renewable generation falls: according to the International Energy Agency (IEA), 96% of newly installed solar and onshore wind facilities generated power for less than new coal and gas plants would have in 2023.

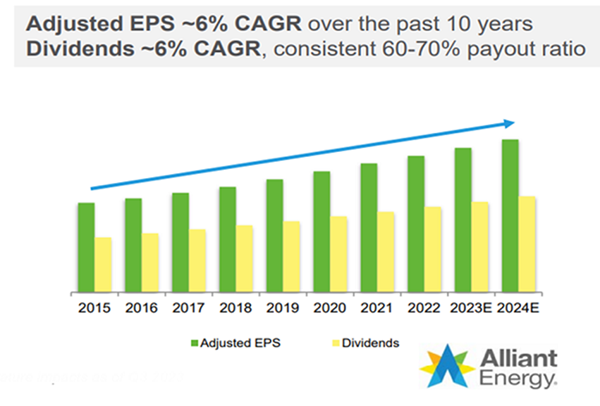

Meantime, Alliant does nothing but make money, having grown EPS at a compounded annualized rate of 6% in the last decade, with the dividend riding shotgun.

Other “dividend digits” work for us here, too: LNT yields 3.9%, and those hikes you see above have resulted in an 88% overall increase in the payout in the last decade.

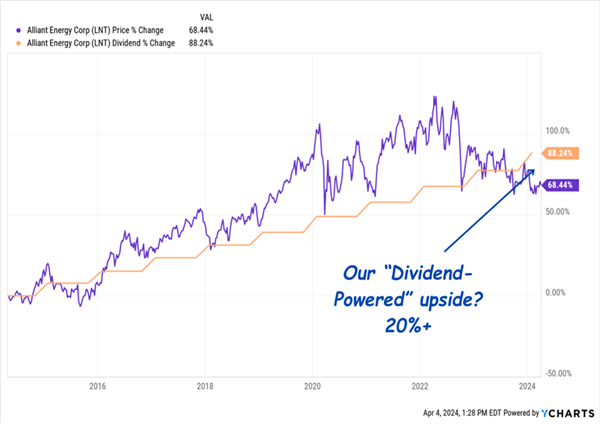

That’s paced the stock higher, point for point. And as with NextEra and Sempra, the stock has fallen behind its payout growth lately, opening up a buying opportunity.

Another “Dividend Gap” Set to Vanish

The P/E agrees, at 16-times forward earnings, well below the five-year average of 19. Long-term debt of $9 billion, also a reasonable 53% of assets douses any concerns about stubborn interest rates, too.

That’s important because as you can see above, a “dividend gap” like this is a rare occurrence for Alliant. And history tells us the price is overdue to bounce back up over the payout—where it almost always resides. The time to make a move is now, before that happens.

Buy Alert: 5 “Rate-Proof” Dividends Set to Return 15% Yearly (Forever)

The strategy we’re using here—buying utilities before rates pop, but focusing only on those with healthy balance sheets—is absolutely critical in rate-obsessed markets like today’s.

By focusing on stocks with overlooked advantages (like healthy balance sheets, rising R&D spending and well-timed share buybacks), we can profit from today’s top trends while giving ourselves a buffer in case things take an unexpected turn.

This is exactly the approach I’ve used to pick 5 other stocks I’m urging all investors to buy today. These 5 picks are all growing payouts quickly and have strong “Dividend Magnets” taking their stocks along for the ride.

This post originally appeared at Contrarian Outlook.

Category: Dividend Stocks