Best Investments In A Rising Interest Rate Environment

Investing and Interest Rate Questions – Answered

Investing today is undergoing a changing market environment. Interest rates are rising and the stock and bond markets are volatile. Wondering how to invest wisely in a rising interest rate environment? Discover how interest rates affect different types of investments, such as stocks, bonds, real estate, and savings. Find out how to protect your investments from rising interest rates and how to invest in a volatile market.

What are the best investments in a rising interest rate environment?

The best investments in a rising interest rate environment are likely to benefit from higher interest rates or are less sensitive to rising interest rates.

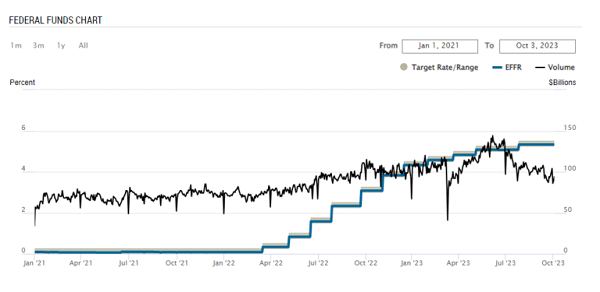

After more than a decade of historically low interest rates, inflation has skyrocketed, and the Federal Reserve Open Market committee has been raising interest rates in an attempt to lower inflation to its target two percent range. The Fed Funds interest rate ultimately drives most interest rates such as mortgages, car loans, credit card debt, bond yields and high yield cash interest rates.

Now, previously out-of-favor cash and bond investments are becoming interesting, as they raise rates and deliver higher returns.

Fed Funds Interest Rate Jan 2021 through Oct 2023

5 Best Investments for Rising Interest Rates

1. Cash and Cash Equivalents

Cash and cash equivalents aren’t typically considered investments. But, during a high interest rate environment, cash can be a wise investment strategy. You’ll lock in relatively high returns, with little or no risk to your principal cash.

Cash and cash equivalents for a high interest rate environment include:

- High yield savings accounts – Available through online and traditional banks.

- Certificates of deposit (CDs) – Available through banks and investment brokerage firms like Schwab or Fidelity.

- High yield money market mutual funds – Available through investment brokerage firms.

- Treasury Bills – Buy them directly from TreasuryDirect.gov or through your investment brokerage firm.

- Commercial paper or very short term debt funds – Ultra-short term debt ETFs increase payments as interest rates rise.

Why Invest in Cash?

These investment might be a regular portion of a diversified investment portfolio, and a ballast for riskier stocks, bonds, and real estate investments. Or, cash and cash equivalents can be the home for your three to six months emergency cash fund and intermediate-term cash needs.

2. Short Term Bond or Debt Funds

A short-term debt fund is a type of mutual fund or Exchange Traded Fund (ETF) that invests in debt securities or bonds with short maturities, typically less than three years. These funds might own various debt securities such as government or corporate bonds.

Short-term debt funds are considered lower-risk investments because their value is less sensitive to changes in interest rates than longer term debt.

Short-term debt funds are a solid way to capture current and rising cash flow from low-risk bonds. Understand that the principal value of your investment might vary a small amount as interest rates rise or fall.

Here’s a quick tutorial on how interest rates impact bond and bond fund prices:

How Do Interest Rates Impact Bond or Debt Prices?

- A bond fund’s value increases or decreases with changes in interest rates.

- How much the bond fund will increase or decrease depends upon it’s duration Typically, a bond with a 3 year duration is expected to decline 3% in value, when interest rates increase one percent, and vice versa.

- The longer a bond’s duration, the more sensitive its price will be to changes in interest rates. This is because longer-duration bonds have more future cash flows that can be affected by rising or falling interest rates.

- For example, if interest rates rise, the price of a longer-duration bond will fall more than the price of a shorter-duration bond. This is because investors will be able to buy new bonds with higher interest rates, making the older, lower-yielding bonds less attractive.

- Conversely, if interest rates fall, the price of a longer-duration bond will rise more than the price of a shorter-duration bond. This is because investors will be able to buy older bonds with higher yields, making them more attractive than new bonds with lower yields.

Why Invest in Short Term Bond Funds?

Short term bond funds are useful in rising interest rate environments for intermediate term financial goals or for the fixed income portion of a diversified investment portfolio. Short term bond funds also produce increasing cash flow, as interest rates rise. Both short and longer term bond funds offer future capital appreciation potential when interest rates decline.

3. Financial Stocks or Sector Funds

A financial stock is part ownership in a financial company who makes money through lending. Banks and financial firms use depositors money to lend to borrowers at higher interest rates. For example, a typical bank savings account today might pay one percent interest on a traditional savings account. The bank turns around and lends the depositors money to a home buyer for 6% mortgage loan. The difference between the 1% that the bank pays to savers and the 6% they receive from borrowers is profit (less expenses). With higher interest rates, the banks spread or profit margins grow. This increases the financial companies profitability and growing profits typically lead to rising share prices.

By investing in the financial sector, you’ll have an opportunity to benefit from the banking industries increasing profits.

Why Invest in Financials?

Lenders like high interest rates, because they can charge higher interest rates on new loans. When rates were near zero, it was difficult for lenders to make a profit. Mortgage and bank lenders receive higher interest payments as rates rise.

Although, banks pay higher interest to savers, typically checking accounts don’t pay interest, and standard savings account interest payments don’t rise as much as loan rates do. This widens the spread or profit margins between interest earned and interest paid. by banks and financial companies, which in turn benefits shareholders with capital appreciation.

4. Floating Rate Bond Funds

Floating-rate bonds and bond funds have interest rates that reset periodically, typically based on a short-term benchmark interest rate. Consequently, their yields can rise as interest rates rise. During rising interest rate environment, a floating rate bond fund provides investors with increasing cash flow. These are ideal investments for those who believe that rates will continue to rise.

A drawback to floating rate bond funds is that when yields decline, cash flows also tend to drop, quickly. When rates start to decline, it might be time to switch from a floating rate to an intermediate term bond fund.

Why Invest in Floating Rate Bond Funds?

These funds typically have very short durations. That means the cash flows quickly respond to changes in interest rates. When interest rates increase, the fund will rapidly reinvest in higher yielding short term bonds, providing investors with higher yields and larger cash flows.

It is important to note that no investment is risk-free, and there is no guarantee that any investment will perform well in a rising interest rate environment. It is important to do your own research and consider consulting with a financial advisor before making any investment decisions.

5. Treasury Bills

Treasury Bills, or T-Bills for short are debt issued by the U.Ss government’s Department of the Treasury. They have maturities that range from several days to one year. Like all bonds, they are loans. And when you buy a T-Bill, you’re lending money to Uncle Sam. They are sold at auction at a discount, and upon maturity, you’ll receive the full value. You can buy them through Treasurydirect.gov or from most major investment firms.

If you buy a 13 or 26 week T-Bill, you’ll get a market interest rate, currently in the five percent range.

Why Invest in U.S. Treasury Bills?

They are the safest debt investments and backed by the U.S. Government. T-Bills are short term, and when interest rates are rising, you can continue to buy new issues at higher rates. They’re easy to buy either through your investment firm or online at Treasurydirect. The T-Bills are state and local tax-exempt, so you’ll only pay federal tax on the interest payments, not state or local tax.

FAQ

How do I get the best interest rates on my savings?

Shop around. There are many high yield savings accounts available today. Compare rates online. Consider an online bank’s high yield savings account, which frequently can beat savings account interest rates due to lower overhead costs.

Some even offer transfer bonuses if you transfer enough savings to the account. Fortunately, most high yield savings accounts will increase your rate as interest rates rise. If you can tie up your money for a few months or more, you might consider a Certificate of Deposit, or CD, which typically offers higher yields than some savings accounts.

How do interest rates affect my savings?

When interest rates increase, the interest paid on your savings account will usually rise as well. This will provide greater returns on the same amount of money.

Bank savings accounts can be tricky. Banks offer many types of savings accounts with different interest rate payment schedules. Standard savings accounts usually offer lower interest payments than high yield bank savings accounts. So make sure to ask your bank to transfer your savings on the highest yield savings account. Or consider an online bank, which frequently surpasses savings account interest rates due to lower overhead costs.

What are inflation-protected investments?

The federal government offers two savings bond investments that promise to protect your cash from the ravages of inflation, TIPs and I Bonds. TIPs bonds are issued with a set interest rate, which is paid on the principal value of the bond. When inflation rises or falls, so will the principal value of the bond, and interest payments will be made on the new adjusted principal value. I bonds are issued with a set interest rate. Every six months, investors are paid the set interest rate, plus an additional interest rate that will increase (or decrease) along with the inflation level.

TIPs can be bought at treasurydirect.gov or though a TIPs ETF. I Bonds can be bought at treasurydirect.gov, and are limited to a $10,000 purchase per year per Social Security number. Investors can also buy an additional $5,000 worth of I bonds with their federal tax refund.

How do I protect my investments from rising interest rates?

If there were a perfect investment solution, it would be diversification. Various investments perform well at different times. For example, when one investment asset declines, a diversified portfolio will own others that will hold steady or rise in value. Rising interest rates remind investors that owning bonds and cash can benefit your portfolio. Rising interest rates reward cash and short term bond holders with growing cash flow.

Investors in financial markets need to understand the price you pay for higher long term returns is the risk of occasional declines in portfolio values. The best way to protect investments from rising interest rates is to set a reasonable asset allocation, in line with your goals and risk tolerance, and rebalance it when the percentages deviate from the target. You’ll smooth out the price volatility of your investments.

How do interest rates affect bonds?

Bond values move inversely to interest rates. When interest rates go up, bond values decline. When interest rates fall, bond values rise. The amount of the increase or decrease in bond values, due to interest rate changes, can be approximated by duration. Duration is a measure of a bonds sensitivity to interest rates and is expressed in years.

For example a bond or bond fund with a duration of 5 years, will be expected to rise in value 5%, when interest rates decline 1%, and vice versa. When interest rates are increasing, it’s best to keep bond maturities and durations shorter, to minimize the bond price declines due to rising interest rates. Shorter maturity bond funds also benefit with greater cash flow, as interest rates increase.

Best Investments in a Rising Interest Rate Environment Wrap up

Rising interest rates are a boon for savers and those with cash. With higher interest rates you’ll profit from greater cash flow on your existing cash or short term bond fund. Cash, cash equivalents, short term debt, and financial securities are four investments that tend to profit when interest rates rise.

Stay away from long term bonds and bond funds, as interest rates go up, as these investments will tend to decline in value. Although when interest rates reverse course and start to decline, your existing bonds and bond funds will benefit from capital appreciation as their prices increase.

It is important to note that investing is always risky, and there is no guarantee of profits. Don’t forget to do your own research and consult with a financial advisor before making any investment decisions.

This post originally appeared at Barbara Friedberg Personal Finance.

Category: Stocks