Six Yields Up To 12% That Wall Street Can’t Stand

It’s hard to find a hater right now.

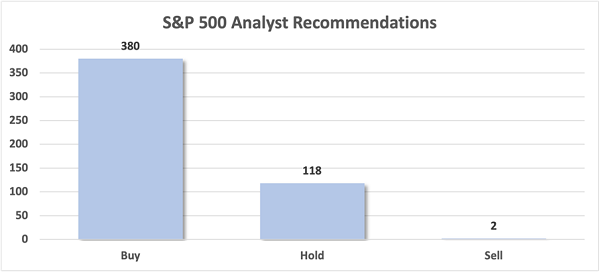

Wall Street fanboys analysts have Buy ratings on more than 75% of the S&P 500 at the moment.

Give us the Sells. That’s right. We contrarians are not afraid to dumpster dive for dividend value!

Today we’ll slam a six-pack of analyst pans yielding between 6.1% and 11.8%. We searched far and wide for these loathed names because, as I write, there are but two blue chips in the Sell bin:

2 Sells Out of 500… What are the Odds!

Sells are where the party is at. Think about it—every subsequent rating change is an upgrade from here.

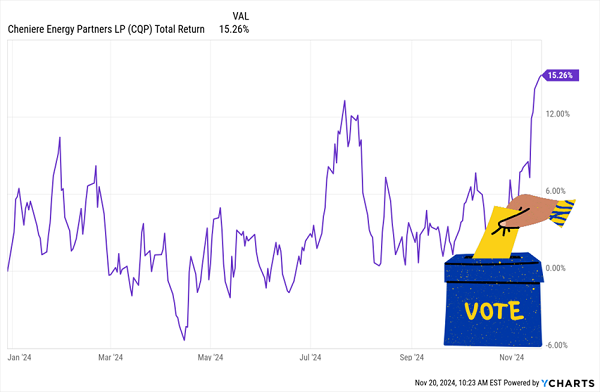

First up is Cheniere Energy Partners LP (CQP, 6.1% yield), which we discussed back in August.

CQP, a subsidiary of Cheniere Energy (LNG), owns the Sabine Pass LNG (liquefied natural gas) terminal in Louisiana, which includes production, storage, and vaporizer facilities, as well as marine berths. It also owns the Creole Trail Pipeline, which connects the Sabine Pass terminal with other pipelines.

Cheniere Energy’s midstream entity has mostly floundered over the past year, largely because of that Sabine Pass terminal. CQP is looking to undergo a massive expansion, but it doesn’t expect to receive approvals until at least 2025. In the meantime, CQP has gone into savings mode to finance said expansion, which took its toll in the form of a significant reduction to its variable distribution earlier this year—and that payout hasn’t bounced back yet.

Not much has changed since then, and Wall Street remains sour on the name, with eight pros calling it a Hold, and another eight rating CQP shares Sells.

However, rising LNG prices and an incoming administration that’s expected to be even more acquiescent toward energy firms have put some pep in Cheniere Energy Partners’ step.

An Election Pop for Cheniere

On the “sad retail” side we have Kohl’s (KSS, 11.7% yield). This stock is hated but for good reason—it’s stock is as dead as its stores.

The core business continues to deteriorate. Its most recent earnings report included a 5.1% year-over-year drop in quarterly comparable-store sales and a 4.2% decline in net sales, and the company expects the latter will be off 4% to 6% for the full year.

The nearly 12% headline yield is spectacular, except that it likely is not sustainable. Kohl’s is already funneling 80% of profits into the dividend. This payout ratio will get worse as earnings continue to deteriorate. Kohl’s shares have lost nearly three-quarters of their value over the past three years and the downtrend should continue.

Analysts also have no love for Western Union (WU, 8.7% yield), either—it has just two Buys against 11 Holds and six Sells.

Here at Contrarian Outlook we last called Western Union a “show me” stock, and for a minute, the once-great money transfer and payment services firm was showing us a little something. But shares have gone back to their losing ways.

It’s not hard to see why. WU is way behind the technological 8-ball. Names like PayPal, Venmo and Zelle have zipped ahead while Western Union has largely been stuck in the past. It’s not for lack of trying—the company has an initiative called “Evolve 2025” in which it’s rolling out new products, improvements and an operational efficiency program. It’s also expanding its digital wallet offerings in Mexico and Singapore.

However, any real growth remains elusive, with the company tracking just 2% revenue expansion by 2025.

Western Union’s Top and Bottom Lines Have Suffered the Ax

It’s a shame, too. WU shares offer nearly 9% in annual income on a much more sustainable payout ratio (50%) than Kohl’s. And the stock trades at just 6 times next year’s earnings. It is cheap, but for good reason.

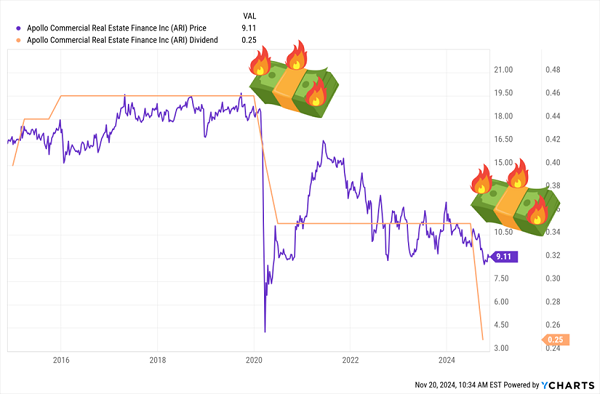

Apollo Commercial Real Estate Finance (ARI, 10.9% yield) is a mortgage real estate investment trust (mREIT) that originates and invests in senior mortgages and mezzanine loans and other commercial real estate (CRE) debt across the U.S. and Europe.

ARI currently boasts a $7.8 billion debt portfolio, 95% of which is invested in first mortgage loans, and 96% of which are floating-rate. Office real estate makes up the biggest chunk of loans, at 23%. But it’s a well-diversified holdings list that includes hotels at 21%, retail at 18%, residential at 16%, and the rest spread around industrial, healthcare, mixed-use and other loans.

Apollo has some promise in the form of improving originations, but the company is in a weak position (and off more than 20% YTD) thanks to a number of troubled assets that it’s working to churn through. That has Wall Street unimpressed with the name, issuing six Holds and one Sell, while three covering analysts refuse to put out an opinion on the stock at all.

Most troubling for us income investors is that, just a couple months ago, Apollo Commercial Real Estate Finance announced a 29% dividend cut, from 35 cents per share to 25 cents.

That’s ARI’s Second Big Cut in Four Years

The move puts its still-very-high-yielding payout on much sturdier ground, sure—but it also signals potential weakness from declining interest rates.

That’s right. While declining rates should in theory help mREITs, I’ve written before that this isn’t always the case. In September, ARI said its payout cut “reflects the impact to operating earnings from ARI’s focus loans as well as anticipated declines in floating interest rate benchmarks as indicated by the forward curves.”

Apollo in theory has potential, but it could remain stuck in the mud for as long as it works through its watchlist loans and other troubled assets.

SLR Investment (SLRC, 10.0% yield) is a business development company (BDC) that invests mostly in senior secured loans of private U.S. middle market companies.

That sentence could be used to describe many BDCs, but SLRC does play in some specialty niches. As of the most recent quarter, its portfolio looked like this:

- Cash-flow loans (traditional sponsor finance business): 22% of portfolio at fair value

- Asset-based loans: 35%

- Equipment financing: 33%

- Life science loans: 8%

- Equity and Equity-Like Securities: 2%

It’s also extremely well-diversified, with roughly 800 issuers across 110 industries, coming out to average exposure of just 0.1% per issuer.

The pros are not enamored with SLRC. It currently earns just two Buys versus five Holds and two Sells (and one covering analyst doesn’t have a Buy/Hold/Sell call on the stock). But that bearishness is largely built on the unknown. SLRC has been acquiring more specialty finance portfolios—most recently, it bought Webster Bank’s Commercial Services division—and those acquisitions will take time to prove themselves out. Also, even Wall Street professionals aren’t quite sure how SLRC’s portfolio, which has a decent 35% chunk of fixed-rate investments, will handle declining interest rates.

But it’s possible that the pros are too negative on the name. I’ve previously pointed out that SLR Investment has trailed the industry for some time, but that track record is at least improving on the back of better-than-expected quarterly results. And SLRC shares do offer a 10% yield at a 10% discount to NAV.

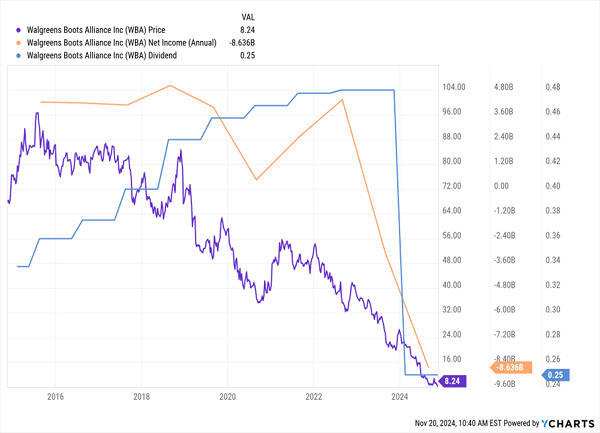

Walgreens Boots Alliance (WBA, 11.8% yield), which yields so much we might mistake it for a BDC, is on Wall Street’s naughty list, too, featuring three Buys versus 12 Holds and four Sells.

It’s unusual to see a name like Walgreens—which many might consider a blue-chip stock—show up on this list. But at this point, Walgreens is a blue-chip stock by reputation only. In 2024:

- Shares have hemorrhaged two-thirds of their value.

- WBA has become a sub-$10 stock.

- Management cut the dividend by 48% (to 25 cents per share), snapping a 47-year streak of payout hikes.

- Standard & Poor’s booted WBA from the S&P 500 Dividend Aristocrats.

- The Dow Jones Industrial Average also expelled Walgreens from its ranks.

Walgreens’ Dividend Finally Catches Up With Its Results

Earlier this year, the ball was in management’s court. Even a little progress, or the reveal of plans that shareholders could get behind, might have given shares some respite. But that hasn’t happened.

Walgreens has largely been focused on cost cuts, and last quarter was no different, with the pharmacy chain announcing it would close 1,200 stores over the next three years. Meanwhile, its debt sits in below-investment-grade territory, and its current-year adjusted earnings are estimated to fall off a cliff this fiscal year.

The only good news (for now, at least) is that the dividend looks relatively safe, insofar as the cut has brought its payout ratio down to the 60%-65% range, even on those now-much-lower earnings expectations.

The One 11% Dividend to Own Now

Walgreens and its 11% dividend might be in the doghouse, but my One 11% Dividend to Own Now is still squarely on the radar.

My One 11% Dividend to Own Now is a rare machine capable of generating a simply ludicrous amount of cash. A 11% yield, in the most practical terms, is:

- Nearly $1,000 a month from a mere $100,000 investment

- $55,000 a year—a proper salary in many parts of the U.S.—from a mere $500,000 nest egg

- A wild $110,000 annually if you have a million bucks to put to work

This post originally appeared at Contrarian Outlook.

Category: Dividend Stocks