Bonds vs Bond Funds – How To Invest In Bonds

What’s the Difference Between Individual Bonds and Bond Funds?

Finally, with interest rates delivering reasonable cash flows, bonds and bond funds are getting exciting. You can make money with bond funds. Two benefits of bonds and bond funds are to stabilize a volatile investment portfolio and to deliver periodic cash flow. Find out the differences between individual bonds and bond funds and learn how to add bonds to your investment portfolio.

Bonds are part of the fixed income asset class. An important trait of these financial assets is the monthly or quarterly bond interest payments. Bond funds and individual bonds are ideal for anyone seeking cash flow and when interest rates fall, the potential for capital appreciation.

What are Bonds and Why You Should Invest in Bonds

Before exploring the difference between bonds and bond funds, it’s helpful to understand what a bond is. In contrast with stocks, which are ownership shares in a publicly listed company, bonds are loans to a company or government entity. In exchange for the loan, you receive periodic interest or coupon payments. When the bond matures, you receive back your initial investment.

The bond interest rate, or coupon payment will vary, based on the maturity or length of the bond and the creditworthiness of the company or government entity. Longer term bonds typically, although not always, pay higher interest rates than shorter term bonds. The highest rated bonds will pay lower interest rates than lower-credit or riskier bonds.

Types of Bonds

Bonds come in multiple varieties including government, government entity, municipal, corporate, and high yield or junk bonds. You can choose to invest in one or multiple types of fixed income bonds and bond funds. Individual bonds and bond funds come in a range of maturities from ultra short-term such as one month, to 30+ year long term bonds.

Government bonds – Issued by the U.S. or international governments to fund their activities. U.S. Treasury bonds come in a variety of forms and maturities including treasury bills, treasury notes, treasury bonds, inflation protected I bonds, and TIPS (treasury inflation protected securities). U.S. treasury bonds are considered the safest bonds because they are backed by the U.S. government. Government bond interest rates or yields are typically lower than those of corporate bonds.

Bonus: Government bonds are exempt from state and local taxation.

Agency bonds – Issued by government entities to finance home buying and other types of activities. Fannie Mae, Freddie Mac, and Ginnie Mae are quasi-government agencies that provide low-cost mortgage loans to consumers.

Municipal bonds – Issued by municipalities and cities to fund their projects. These may be both federal, state, and local tax exempt and good for those in high tax brackets.

Bonus: Most municipal bonds are exempt from federal, state, and local taxation, if they are issued within your state of residence.

Corporate bonds – Issued by companies to finance new or existing projects. The types of corporate bonds depend upon the credit worthiness of the debt and include high grade down to the lowest credit quality, or junk bonds. Riskier junk bonds pay higher interest rates than top rated corporate bonds, because their risk of default is greater.

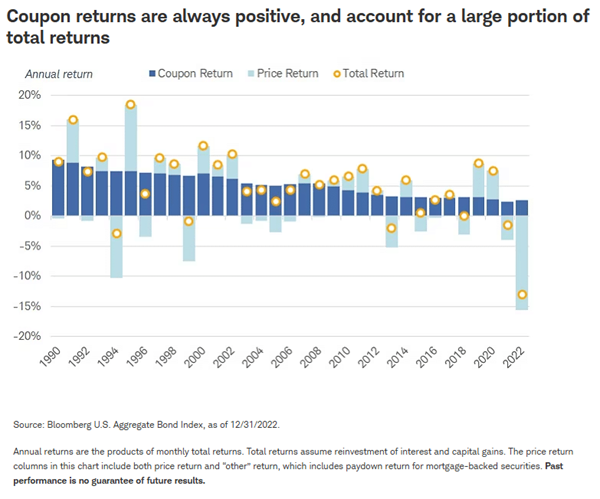

Bond Returns 1990 – 2022

How Do You Make Money With Bonds?

Bond returns depend on a variety of factors. Bonds and bond funds deliver regular interest or coupon payments. Bond funds frequently pay monthly interest payments, while individual bonds deliver quarterly or semi-annual cash flow.

As the chart above illustrates, bond interest or coupon payments are always positive for both individual bonds and bond funds. So, if you don’t sell the bond or bond fund, you’ll be assured of a steady source of cash. But your total return on bonds can be positive or negative, based upon a variety of factors. Fortunately for bond holders, between 1990 and 2022, total returns were negative only five times.

You can make money with bonds two ways:

- Regular interest or coupon payments – Monthly, quarterly or semi-annually interest payments.

- Bond or bond fund appreciation – When interest rates decline, bond values rise (and, vice versa).

Individual bonds, bought at issue and held to maturity will always have a positive return. Although, in contrast with stocks and stock funds, bonds normally deliver lower total returns than stocks, albeit with less price volatility.

Bond Yields – Current Yield, Yield to Maturity and Yield to Worst

Understanding bond yields and ratios will help you gauge your potential returns.

A bond has a coupon or interest rate, which is the percentage rate paid on the face or par value of the bond. If a five-year bond has a face value of $1,000 when issued and a 4% coupon payment, investors will receive $40 per year. You’ll typically receive interest payments quarterly, or $10 four times per year. When the bond matures in five years, you’ll get your initial $1,000 payment back. If you sell the bond before maturity, you will receive more or less than the principal or face value of the bond, depending upon supply and demand, as well as market interest rates.

This example is simple, you receive a four percent annual return on the bond.

A bond fund owns a group of bonds, and so the coupon and term is the aggregate of all of the bonds owned within the fund. But, more about that later.

If you buy the bond on the open market, from your investment broker, it may be worth more or less than the $1,000 face value, depending upon the current interest rates and demand for the bond. You’ll still receive the 4% annual interest payment, but it will be paid on your actual investment, which could be less or more than $1,000. That makes calculating your annual return a bit more complicated.

When any bond matures, the owner receives the par or face value, even if he or she paid more of less for the bond. That adds to the complexity of calculating bond returns.

Bond Funds vs. Bonds – Ratios to Help You Understand Potential Returns

What is the current yield or yield on cost? The current yield assumes that the bond will be held until maturity and is determined by the current market price and the bond’s coupon rate. If a bond is selling for $1,100 on the open market and the coupon rate on the bond is 4%, the current yield is ($40/$1,100) * 100 or a yield on cost of 3.64% annually.

What is the yield to maturity? The bond’s yield to maturity is based upon the purchase price of the bond, face value, coupon rate, maturity, and length of time until maturity. The result of this calculation gives you an idea of the return you’ll receive, given the price you pay today, and assuming you hold the bond until maturity. A bond fund’s yield to maturity includes the aggregate information of all bonds owned within the fund. This information is usually listed with the bond’s information. Yield to maturity assumes that all interest payments are reinvested at the coupon rate.

What is the yield to worst? Given the bond’s purchase price, coupon rate, face value, call features and maturity, the yield to worst is the worst total return that you might receive. Once you buy a bond, your purchase price is set, as is the pre-existing coupon rate. The yield to worst is the lowest possible yield that you might receive from the bond. This will be determined by several factors, if the bond is called (redeemed early) by the issuer, or if you sell it before maturity, and upon redemption, the value is lower than your purchase price, your yield might be lower than expected.

When buying a bond or bond fund, these ratios are usually available on the bond’s information listing.

Bonds vs Bond Funds – What’s the Difference

The difference between bonds vs bond funds is that individual bonds have a set interest rate and maturity date, and bond funds do not. One difference between bonds and bond funds is that the bond fund’s coupon payment amounts, or interest payments will vary as old bonds mature or are sold and new bonds are purchased. Bond funds lack a maturity date. Bond funds also charge a management fee – lower for a bond index fund and higher for an actively managed bond fund.

You might think that buying individual bonds vs bond funds provides more control and better returns, but that isn’t necessarily so. Minus the expense ratio, there is no actual difference between a bond and a bond fund, except that you will receive greater diversification with a bond fund, and frequently better returns, due to the skill of fund managers. A bond fund is simply a collection of individual bonds.

Pros and Cons of Individual Bonds

Bond Pros

- Good savings vehicle for an expected future expense. You know how much interest you’ll receive as well as the final principal payment, if held to maturity.

- Known and steady income stream. When you buy an individual bond, the interest or coupon payment will remain the same.

Bond Cons

- You need a large bond portfolio to realize significant diversification. Some advisors recommend at least $50,000 for individual bond investors.

- Your purchase price for individual bonds will generally be worse than the pricing that bond fund institutional investors receive.

- You need a degree of expertise to research, create and manage an individual bond portfolio.

Pros and Cons of Bond Funds

Bond Fund Pros

- Broad diversification in one fund.

- Low and reasonable management fees are available.

- Professional management can increase total returns.

- Monthly income stream is available.

Bond Fund Cons

- Price at sale may be lower or higher than your purchase price.

- High expense ratios can cut into total returns.

- Bond funds lack a set coupon rate and maturity date.

There are actually two types of bond funds, exchange traded funds or ETFs and bond mutual funds.

What’s the Difference Between a Bond Mutual Fund and a Bond ETF?

Understand whether a bond ETF or bond mutual fund is best for you.

| Feature | Bond Mutual Fund | Bond Exchange Traded Fund |

| Trading | Buy and sell only at the end of the trading day at net asset value (NAV) | Traded throughout the day at market prices, which can vary |

| Investment Minimum | Can have an investment minimum up to several thousand dollars | Investors need less cash and can buy a single share, or even a partial share |

| Fees | Frequently have highish expense ratios/fees, especially if bond fund is actively managed | Usually have lower expense ratios/fees |

| Transparency | Holdings are revealed monthly or quarterly | Holdings are usually disclosed daily, equating to greater transparency |

| Ease of Purchase | May only be sold through specific financial institutions | Can be readily purchased from any investment broker who sells ETFs |

| Commissions | Some mutual fund vendors charge commissions to buy and/or sell shares | Can be purchased and sold commission-free at most investment brokerage firms |

Unless you are seeking a specific strategy bond fund, that is only available as a mutual fund, ETFs usually offer lower fees and easier ways to buy and sell the fund.

Where to Buy Bonds and Bond Funds?

The best place to buy individual bonds is from a major investment broker such as Schwab or Fidelity. They have a fixed income specialist group that can help select bonds, as well as charts, tools and screeners to help you select your bonds. Just be careful of “up selling.” It’s not uncommon for an investment company representative to attempt to sell you fee-based products and services such as investment management or high fee specialty products.

Bond mutual funds can be purchased from the bond mutual fund issuer or from an investment brokerage firm. The investment brokerage firm will not sell all bond mutual funds, but only a selection. There may be commissions to buy and sell the bond mutual funds as well. Fidelity is known to have a large stable of investment mutual funds from which to choose, some are sold commission-free and others are not. Vanguard is also known to offer low-cost mutual funds.

You can also buy government bills, notes, bonds, TIPS and I Bonds at treasurydirect.com.

You can buy bond ETFs from any financial company that sells ETFs. That includes Robinhood and M1 Finance.

Bonds vs Bond Funds – Which are Best For You?

If you have more than $50,000 to allocate to a diversified bond portfolio, and you would like to know exactly how much your cash flow and final bond payment will be, then buying individual bonds make sense. For the rest, bond ETFs and bond mutual funds make much more sense. We prefer the lower cost, and flexibility of bond ETFs over bond mutual funds.

For most investors, except those that are in their 20’s and 30’s and have a high tolerance for stock market declines, it’s a good idea to own some fixed income assets in your portfolio. If you own them in an IRA or 401k, you won’t have to pay tax on the interest payments, and they will add some stability to your investment portfolio. Investors had a difficult time owning bonds during the ultra low interest rate period from 2002 through 2022. Those ultra low and occasionally negative bond total returns were unusual, within the long-term investment environment. As long as market rates remain above 3% or so, adding bonds to a diversified investment portfolio makes sense.

FAQ

Who should invest in bonds?

Anyone who is seeking regular cash flow and potential bond or bond fund appreciation. You might also invest in short-term bond funds if you’re seeking seeking higher yields than those available from cash assets. Adding bonds to a stock portfolio typically moderates the overall volatility of your investments.

How do you make money with bond funds?

You’ll receive monthly cash flow from most bond funds. These payments reflect the aggregate interest or coupon payments of the bonds owned within the fund. You can take these payments as cash or reinvest them into more shares of the fund. When you sell, especially when market interest rates decline, your bond fund might appreciate in value. Of course, the reverse is also true. If interest rates are expected to increase, then buy bond funds with shorter maturities, as bond values move inversely to with interest rates.

What are 5 types of bonds?

The five types of bonds include:

1. Corporate bonds: Issued by U.S. and international companies

2. Government bonds: Issued by the U.S. and foreign governments. U.S. government bond interest is state and municipal tax-exempt.

3. Municipal bonds: Issued by U.S. cities and municipalities. Municipal bond interest may be tax-exempt.

4. Agency bonds: Issued by quasi-government agencies such as FannieMae and FreddieMac. These agencies support citizens by offering lower rate mortgages.

5. Zero coupon bonds: These bonds are issued at a deep discount to face value and don’t pay regular coupon rates. Upon maturity the purchaser receives the full value value of the bond. These zero coupon bonds are typically long term and useful in planning for long term expenses.

What is the face value of a bond?

The face value of a bond is the actual or par value of the bond. This is the amount that the owner will receive at maturity, when the bond comes due. Understanding a bond’s face value is helpful when calculating your expected return.

What is the difference between yield and return?

Yield is on a bond or other investment is determined by the price that you pay and the expected interest or dividend payment. If you buy a bond for $1,000 with a 4.0% interest rate or coupon payment, then your yield is 4.0%. If you bought that same 4% bond in the open market for $1,100, then your yield would be 3.64% or ($40/$1,100) * 100.

The return incorporates the price you paid for the bond, the ultimate value you receive when you sell the bond and all of the cash flows in between less any expenses or commissions. Total Return =( [(End value of the bond + coupon interest + compound interest) – (taxes + fees/commissions)]-[(Beginning investment value or purchase price)]) / Beginning investment value or purchase price and expressed as a percentage. This is the total return of your investment versus the return of the interest payments or yield.

Compared with a short-term investment, what is the general return of a long-term investment?

This question is rather general as returns depend upon the types investments as well as how long the investment is owned. A short term bond investment return is typically lower than that of a long term bond investment. And the returns on each are affected by current market interest rates. in fall 2024, a short term bond fund will pay roughly 4.75% while a long term total bond fund will pay approximately 3.25%. In general short-term investment returns are typically lower than those of long-term investments. But, there is little absolute certainty regarding most returns except for when you purchase an individual bond at issue and hold it until maturity.

This post originally appeared at Barbara Friedberg Personal Finance.

Category: Bonds